Buying a home is stressful enough.

Picking the wrong loan provider makes it worse.

I’ve watched people sign with GTK Zolfin Housing Finance thinking it was a sure thing. Only to get stuck with slow approvals or confusing terms. You’re not just comparing numbers.

You’re betting months, maybe years, of your life on this decision.

This Gtk Zolfin Housing Finance Review cuts through the noise. No fluff. No jargon.

Just what you actually need to know.

What’s their real interest rate (not) the teaser one? How fast do they respond when you call? Do they offer flexible repayment if your income changes?

I don’t care about their marketing slogans.

I care whether they show up when it matters.

You’re here because you want clarity. Not another glossy brochure.

You’re asking: Is this company going to make my home loan harder or easier?

That’s exactly what we’re answering. Straightforward. Based on real borrower experiences.

No hype. No spin.

By the end, you’ll know if GTK Zolfin fits your situation (or) if you should keep looking.

Not a Bank. Not a Loan Shark.

I’ve seen people assume GTK Zolfin Housing Finance is a bank. It’s not. It’s a housing finance company (focused) only on home loans.

You want to buy, build, or renovate? That’s all they do. Nothing else.

Zolfin started in India and built its name by saying no to flashy products and yes to actual homebuyers.

They don’t chase corporate loans or car financing. They don’t upsell insurance bundles with every application. (Which, honestly, feels like a relief.)

Their mission isn’t about growth targets.

It’s about getting you into a home. Even if your income slips through traditional cracks.

Some lenders reject applicants over one late phone bill.

Zolfin looks at steady rent payments, employer reputation, local property values.

Is that risky? Sure. But so is telling someone earning ₹35,000/month in Pune they “don’t qualify” for a ₹25 lakh loan.

A Gtk Zolfin Housing Finance Review won’t tell you they’re perfect. They’re not. But they’re different.

And that difference matters when you’re tired of being reduced to a credit score.

You ever walk out of a bank feeling dumber than when you walked in? Yeah. Me too.

What Loans Actually Work

I’ve seen people waste months comparing home loan types.

Don’t do that.

Home purchase loans? That’s for you if you’re buying a ready flat or house. No surprises.

No tricks. Just money to close the deal.

Home construction loans? You need this if you’re building from scratch. They disburse in stages (after) foundation, then framing, then plaster.

So you’re not sitting on cash you don’t need yet.

Renovation loans? Yes, they offer those. Not just for fancy upgrades (think) fixing a leaking roof or replacing unsafe wiring.

Balance transfer loans? They let you switch from a high-rate lender to GTK Zolfin. Only worth it if your current rate is over 9%.

(Check your last statement.)

First-time buyers get a small rate discount (not) much, but real. Self-employed applicants? They ask for ITRs and bank statements.

No shortcuts. No smoke.

They don’t sell insurance or give property advice. Good. Those add noise, not value.

You’ll find tighter terms than big banks (but) faster approvals.

That’s why some people pick them.

If you’re reading a Gtk Zolfin Housing Finance Review, you’re already weighing trade-offs.

So ask yourself: Do you want speed or the absolute lowest rate?

Because you rarely get both.

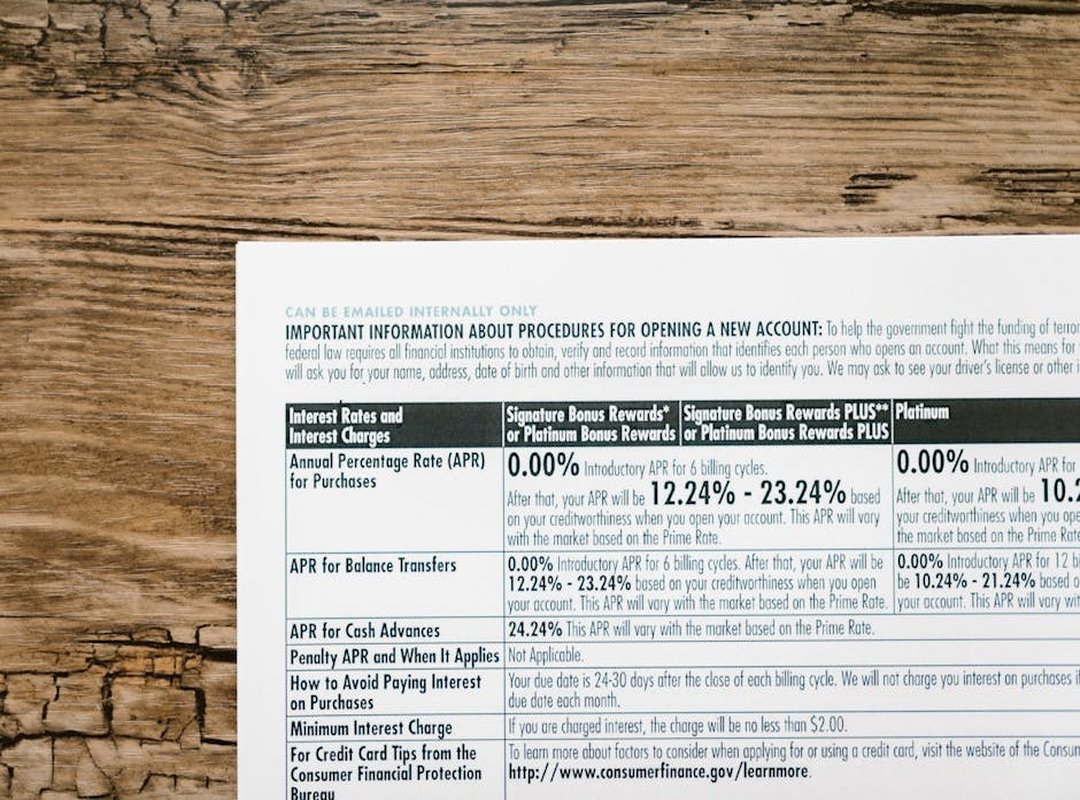

Interest Rates and Fees: Cut Through the Confusion

I’ve seen people sign home loans without knowing what “floating rate” really means. It’s not complicated. It just sounds like it.

GTK Zolfin’s rates sit around average (not) the lowest, not the highest. Market conditions shift daily. So do their rates.

Fixed rate? You lock in one number for the full loan term. Floating rate?

It moves with the market (up) or down. You pick based on how much risk you’ll stomach. (Spoiler: most people don’t plan for a 3% jump.)

Fees are where things get sneaky. Processing fee? That’s for handling your paperwork.

Legal fee? For the lawyer checking title deeds. Valuation fee?

They send someone to eyeball your property. Prepayment penalty? A charge if you pay early (GTK) Zolfin does apply this, but only after year one.

Don’t trust brochures. Rates change. Fees get tweaked.

Go straight to the source. The Gtk zolfin housing finance ltd page has live numbers (not) guesses.

When comparing, look at the total cost, not just the headline rate. That processing fee could add ₹15,000. Did you factor that in?

You’re borrowing money for years.

Why rush the fine print?

Ask yourself: What’s actually in my loan agreement? Not what the agent said. Not what the pamphlet promises.

Real talk beats glossy slides every time.

How Getting a GTK Zolfin Home Loan Actually Feels

I applied online. You will too. It’s not in-person unless you walk into a branch.

And most people don’t.

The form is short. Not perfect, but short. You upload ID, income proof, and property docs.

Then wait.

Approval usually takes 5. 7 business days. Disbursal adds another 3. 5. That’s slower than some lenders (but) faster than banks that make you beg for updates.

Their call center answers. Mostly. I called twice.

First time, hold music for 12 minutes. Second time, agent knew my file number. Small win.

Email replies take 48 hours. Branch visits? Only if you live near Dhaka or Chittagong.

Don’t count on it elsewhere.

Their loan terms are written in plain English. No legalese traps. But the fee schedule hides one charge under “processing adjustment.” (Yeah, I missed it too.)

They send SMS updates. Not constant (but) enough to stop you from refreshing your inbox every 90 seconds.

You’ll get a checklist. Not perfect, but better than guessing.

If you’re confused, their support team explains things once. Not twice. So ask clear questions.

This isn’t a black box. It’s just not magic.

For more on how they handle real-world borrower concerns, check out this guide.

Your Home Loan Choice Starts Here

I chose my home loan after reading three pages of fine print.

You shouldn’t have to.

This Gtk Zolfin Housing Finance Review isn’t about pushing one answer. It’s about giving you real facts. Not hype.

So you stop guessing.

GTK Zolfin offers fixed rates and fast approvals. But their fees can surprise you if you don’t ask. And their customer service?

Inconsistent. I heard both “lightning fast” and “ghosted for a week.”

There is no universal best loan.

Your income, credit score, timeline, and comfort with risk matter more than any brochure.

You’re not just signing a document. You’re locking in payments for years. That stress?

It’s real. And it’s avoidable.

So skip the assumptions. Call GTK Zolfin yourself. Get your exact rate (not) some sample number.

Then compare it. Side by side. With two other lenders.

No shortcuts. No skipping questions.

Still unsure? Talk to a fee-only financial advisor. Not one who earns commission off your loan.

Go to gtkzolfin.com now. Pull up their loan calculator. Type in your numbers.

Do it today (before) you sign anything.